Millions of American consumers are in for a jolt: a backlog of household debt that could abruptly come due in the months ahead.

One of the less-noticed pillars of financial relief during the COVID-19 pandemic has been temporary debt relief, a process known as “forbearance.” It allowed people to postpone payments on $2 trillion worth of home mortgages, car loans, student loans, and other debt.

A new study, coauthored by Amit Seru at Stanford Graduate School of Business, finds that this temporary debt relief did a great deal of good. It prevented a wave of home foreclosures and shielded millions of people who had lost their jobs but still had big student debt. Indeed, it may have helped prevent a collapse in housing prices that could have wiped out vast amounts of household wealth.

The urgent issue now, says Seru, is what to do about the avalanche of past-due bills when the forbearance ends.

$70 Billion in Missed Payments

Drawing on nationwide credit bureau data, the study estimates that some 50 million people postponed about $43 billion in loan payments between March and October of last year. By the end of March 2021, the researchers predict, 60 million people will be $70 billion behind on their payments.

Most of those looming bills are tied to home mortgages ($3,200 on average, as of last fall), car loans ($430 on average), and student loans ($140 on average).

“For many households, the missed payments add up to a huge part of their monthly income,” Seru warns. “Depending on how you unwind that debt, we could have a huge drag on the economy, just as we had after the Great Recession — the economists Atif Mian and Amir Sufi documented that, and I have written about it too. It took the Obama administration seven or eight years to get past that.”

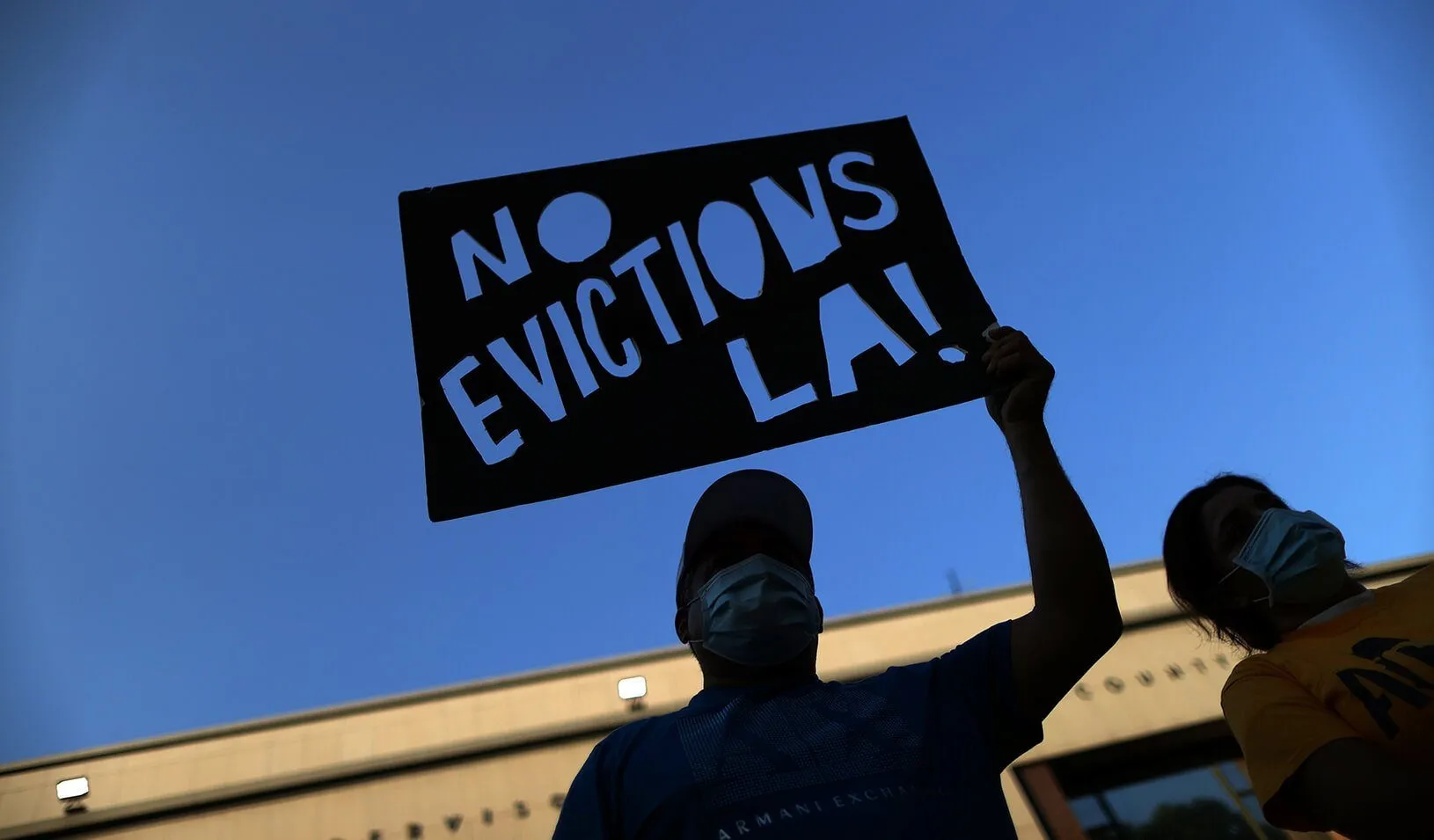

There are no painless answers, Seru says. If lenders insist on immediate repayment as soon as the forbearance period ends, millions of families may have to choose between keeping their houses and paying for basic necessities.

If lenders decide to spread out repayments over months or years, many of them could insist on adding accrued interest to cover the delay in repayment. Under current law, lenders would be entitled to such accruals, and banks would likely object to being asked to shoulder a public burden on their own. The federal government could subsidize the delayed payments, but that would most likely require congressional legislation.

Who’s at Risk?

The new study lays bare both the amounts of money involved and the kinds of people who could soon be hit with a new financial shock.

When the full fury of the COVID-19 pandemic hit the United States last year, Congress required lenders to allow borrowers to delay payments on federally insured mortgages and student loans. In addition, the study finds that many private lenders voluntarily agreed to provide forbearance on a wide range of other mortgages, car loans, and credit card debt.

To quantify the magnitude of that relief and the challenge ahead, Seru teamed up with four researchers: Erica Jiang at the USC Marshall School of Business; Gregor Matvos at Northwestern University’s Kellogg School of Business; Tomasz Piskorski at Columbia University; and Susan Cherry, a PhD student in finance at Stanford.

The team used a detailed dataset from Equifax, the credit reporting agency, that covered 20 million borrowers. The data didn’t reveal people’s names, but it did provide credit scores, payment histories, delinquencies, deferrals, and borrowers’ geographic locations. From that, the researchers estimated the nationwide totals and the kinds of people who got help.

By and large, the researchers found, forbearance provided relief to people who truly needed it. Consumers with above-average incomes did account for a higher share of the total dollar value of missed payments, because people who earn more generally take out bigger mortgages — and many of them faced hardships due to lost employment. But lower-income people signed up for relief in much higher numbers. So did people in localities with large populations of Blacks and Hispanics, who were hit hard by the pandemic, as well as people in areas with high COVID-19 infection rates.

The study also finds two interesting patterns related to how much relief was administered. Only 10% of eligible borrowers actually requested debt relief, which Seru says indicates that the relief went to those who truly needed it. In addition, one-third of those who were given forbearance actually kept making payments. They appeared to use the relief like a credit line that they could draw on if their situation became dire.

Protecting the Housing Market

Seru and his colleagues found that forbearance reduced financial stress for many households. Delinquency rates on consumer loans actually dropped significantly, from 3% just before the pandemic to 1.8% later last year.

Perhaps more striking, the economic collapse didn’t lead to a tsunami of home foreclosures, which could easily have caused a collapse in housing prices. After the mortgage meltdown and the Great Recession of 2008 and 2009, Seru notes, home foreclosures in particular neighborhoods often sparked a chain reaction of falling prices and more foreclosures in the surrounding areas. That aggravated what was already the worst economic downturn in a century.

By contrast, home prices have actually spiked up since the pandemic arrived. Forbearance could be one of the reasons. About 7% of people with home mortgages entered forbearance agreements last year. By contrast, only 2% did so during the Great Recession.

“In 2007, the immediate and perhaps largest focus of policymakers was on the banking side — on how to get banking going again,” Seru notes. “It was more than a year before they started somewhat addressing the household side, and by then it was too late. This time around, the administration was swift to rightly address the household side.”

Unfortunately though, Seru warns, many of the problems have only been postponed.

“We have to get going on these issues right now. We have to be careful in how we unwind this forbearance overhang,” he says. “We have the data, and policy makers need to get on how they would design such a policy. The issue of renegotiation with borrowers is difficult; it requires customization to each consumer’s situation, which requires data and can take weeks or months to design. In the meantime, many consumers could find themselves locked out of their houses. A chain of delinquencies could quickly emerge.”

For media inquiries, visit the Newsroom.