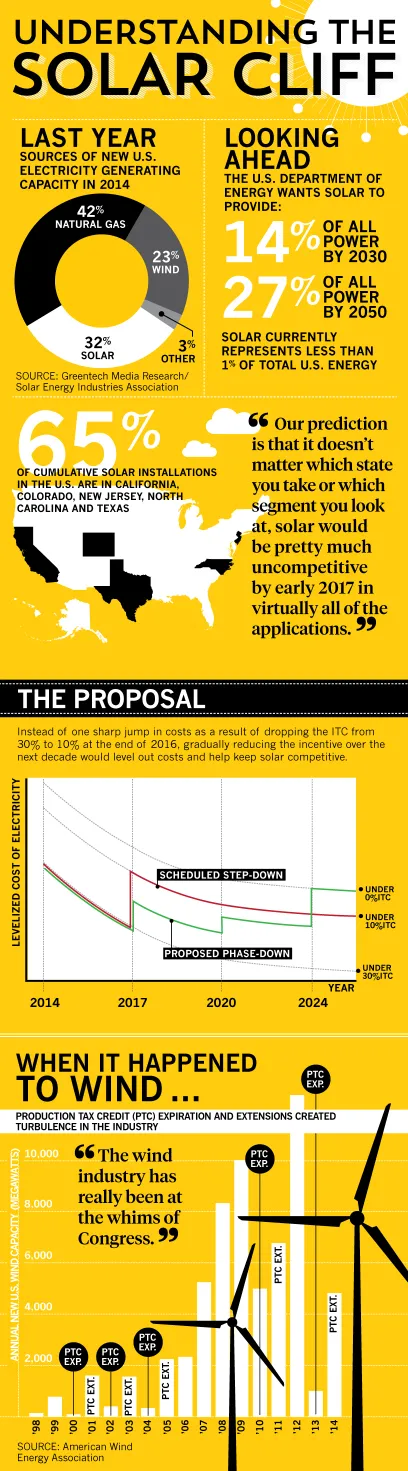

The prospects for the widespread adoption of solar power are sunnier than ever. Thanks to incentives and plummeting costs, the solar photovoltaic industry is experiencing dramatic growth, accounting for almost a third of new generating capacity in the U.S. in 2014, second only to natural gas. The U.S. Energy Information Administration projects an increase of 6 gigawatts of utility-scale solar capacity by the end of 2016 (for comparison, the Hoover Dam has a maximum output of 2 GW of capacity). Apple recently announced plans to invest $850 million in a utility-scale facility in California while Google dropped $300 million into a SolarCity fund to finance residential solar installations. The U.S. Department of Energy wants solar to provide 14% of the power in this country by 2030 and 27% by 2050, up from less than 1% today. It’s a steep road, but momentum is clearly building.

The problem is, unless there is a change to current legislation, the solar power industry in this country is headed for a cliff.

A federal tax incentive for solar projects called the Investment Tax Credit is set to expire at the end of next year. That will be a substantial blow to the industry as it’s learning to stand on its own, says Stanford professor Stefan Reichelstein. His new study, coauthored with research associate Stephen Comello, examines why this tax incentive is so important and offers up an alternative that would steer us away from the cliff.

The Solar Credit Success Story

Designed to support the widespread deployment of solar energy, the Investment Tax Credit was created as part of the Energy Policy Act of 2005 and extended for eight years in the Emergency Economic Stabilization Act of 2008. Specifically, the ITC allows companies that install, develop, or finance solar systems to claim a tax credit in the amount of 30% of the investment cost of the project.

The ITC helped to spur demand for solar installations, which in turn drove down costs. “The magnitude of the tax credit is very substantial and has given a boost to the solar industry in the U.S.,” Reichelstein says. “Also, the solar industry is cooking not only here in the U.S. but also in many other countries that have their own incentive systems. In terms of worldwide deployments, solar power is on a steep growth curve and there is no sign of it letting up.”

However, the 30% credit that has been so instrumental in jump-starting the industry in the U.S. is in effect only until Dec. 31, 2016, at which point the credit for commercial developers, who pay corporate income taxes, will drop to 10%. Individual homeowners who wish to self-finance would not receive any federal credits on their personal income taxes beyond 2016.

Clouds on the Horizon

That drop would be a sharp setback to solar’s progress in becoming cost-competitive with other energy sources, Reichelstein shows in his study, “The U.S. Investment Tax Credit for Solar Energy: Alternatives to the Anticipated 2017 Step-Down.”

To assess the cost competitiveness of solar photovoltaics, the researchers analyzed the “levelized cost of electricity,” or LCOE, a metric used to compare the lifetime costs of different electricity generation sources.

The researchers started by examining the economics of solar photovoltaics in five states that account for more than 65% of the solar installations in the U.S. — California, Colorado, New Jersey, North Carolina, and Texas — and across three market segments: residential, commercial, and utility-scale. Considering only the federal ITC, their results revealed a varied landscape of cost competitiveness relative to the rates charged by energy service providers. In California, for instance, residential and commercial solar installations are easily competitive with retail and commercial rates respectively. In Colorado, North Carolina, and Texas, solar installations are close to breaking even with those retail rates. On the other hand, utility-scale solar installations, which have to compete with lower wholesale electricity prices, are not yet competitive in any of the segments.

While under these circumstances solar hasn’t reached “grid parity” yet, the researchers forecast a brighter future. Manufacturing costs for solar panels and installation costs have plummeted as the technology has matured in recent years. Projecting continued cost reductions to the end of 2016, the researchers found that solar is poised to make significant gains in cost-competitiveness across the entire sample.

But those projections look different if the ITC were to drop to 10%. “Our prediction is that it doesn’t matter which state you take or which segment you look at; solar would be pretty much uncompetitive by early 2017 in virtually all of the applications,” Reichelstein says.

Avoiding the Cliff

A preferable strategy to dropping the solar tax credit from 30% to 10% and leaving it there in perpetuity, the researchers argue, would be to institute a more gradual phase-down starting in 2017. Comello and Reichelstein suggest that the government could drop the credit in smaller increments, first in 2017, a second time in 2021, and then eliminate it after 2025. Under their phase-down proposal, investors would be eligible for targeted tax credits, calculated either as lump-sum amounts or percentage-based tax credits that would be phased down from 30% to zero.

“That 10% ITC is still a considerable incentive that should not be minimized in terms of impact,” Reichelstein says. “Under the current tax rules, the industry would take a significant hit in 2016, but then keep significant subsidies. Our thinking was, why do the sharp step down and then support the industry forever if it doesn’t need it forever?”

Instead of falling off a cliff, the industry would instead have to weather a series of smaller shocks as it works through a critical developmental phase. The researchers’ findings suggest that the industry should be able sustain its momentum through those smaller shocks, leaving it poised to achieve true cost competitiveness by 2025.

“By that time, if history is any guide, solar should be fully competitive with natural gas or other energy sources at least in favorable locations,” Reichelstein says.

And the quid pro quo aspect could make the proposal an easier pill to swallow politically. Under the alternative proposal, taxpayers would be spending more in the immediate on solar, but they would no longer be supporting the industry in perpetuity.

“It has a little bit of the flavor of Saint Augustine’s prayer, ‘Lord, give me temperance and chastity, but not right now,’” he says.

An Urgent Matter

A change to a tax credit could kill the nascent industry. | Illustration by Shannon May

Although the cliff is nearly two years off, we should resolve the issue now, Reichelstein says. For one thing, it would help ensure the industry doesn’t mirror the wind industry, which suffered whiplash as incentives expired and were renewed at the last minute multiple times over the past decade, contributing to a “prolonged market contraction” in that industry.

“The wind industry has really been at the whims of Congress,” Reichelstein says. “So putting solar on a long-term footing would be helpful for suppliers and consumers in the industry so they can plan farther out.” Otherwise, he says, “it’s very likely that running up to the end of 2016 we would see a boom followed by a bust with all the costs that come with such a cycle.”

We already see evidence of this boom. Companies like SolarCity are hiring in droves. In fact, according to a report by the nonprofit research group the Solar Foundation, one of every 78 new jobs in 2014 was created by the solar industry. Further, it anticipates that the total employment by the industry will grow over 20% in 2015, to 210,060 workers.

“You can see what would happen in 2017,” Reichelstein says. “Companies like SolarCity may be well-positioned because they are cost leaders. The way they have phrased it is, ‘We’re fighting the step-down, but we will survive.’ But not everybody will survive.”

Greater Market

Still, the U.S. is only one country that accounts for less than 10% of the global solar market, whereas China, which has historically dominated solar panel production, is quickly becoming a leading installer and consumer of solar power.

“The good news to keep in mind is that irrespective of what happens here, the rest of world will continue to expand rapidly with solar deployments,” Reichelstein says. “The question is where that would leave the U.S. solar industry.”

Stefan J. Reichelstein is the William R. Timken professor of accounting and a senior fellow at the Woods Institute for the Environment. He is also faculty research director of the Steyer-Taylor Center for Energy Policy and Finance and faculty director of the Sustainable Business Initiatives.

For media inquiries, visit the Newsroom.